Pension Plan vs. 401(k): The Pros and Cons

June 22, 2022

With such a wide variety of retirement plans available, it is important to understand what these plans are all about and how they differ. If you are careful to utilize your retirement plan correctly, you can create the ideal retirement for yourself and your family. If not, you could be putting that dream at risk.

Because pension plans have become less and less common as 401(k) plans become more widely adopted it is important to dive into why we are seeing this trend. Note: This article is for purely educational purposes to help explain what these two retirement plan types do and the risks and advantages of each.

How They Stack Up

Prior to the 1980s, pension plans were overwhelmingly the most popular retirement vehicle in the United States. This was mostly due to their simplicity: Work for a company, and that company pays you now and for the rest of your life. There were many factors that led to the change in preference from pension to 401(k). We’ll cover the key factors in the paragraphs below.

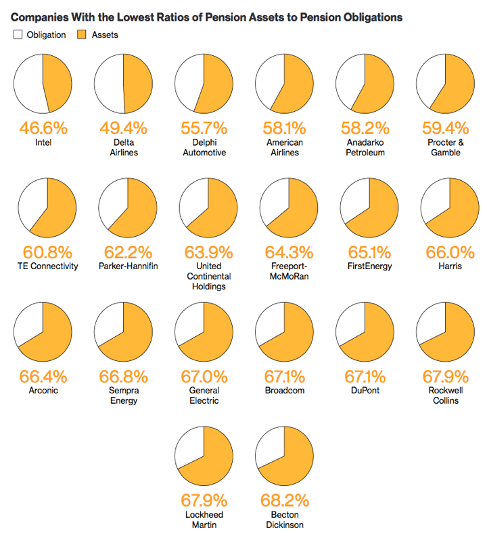

Funding. In the decades following the middle of the last century, the stock market was performing incredibly well, and interest rates were at all-time highs. This was a time when CDs (certificates of deposit) at your local bank were paying double-digit interest, and some bonds were returning nearly 30%. This overly generous market gave pension managers and corporations an inaccurate picture of how much would need to go into a pension plan to fund its obligations. This led to the issues we see today that are affecting pension plans across the country. (See the graph below.)

Control. One of the major differences between a 401(k) plan and a pension is who is responsible for controlling the money in the account. With a 401(k) plan, the employee has total control of the account. Understanding how much it is worth, how it is invested and how to access it is as simple as logging in to your account. On the other hand, pension benefits are an estimated future promise. That promise can change, depending on your employment, the company’s long-term success and the performance of the pension fund account. If the company or the pension managers mismanage the pension plan, your future may be in jeopardy — and you won’t even know about it until it is too late.

Reliability. The most important factor in a pension is the reliability of the income you expect to live off of. A pension’s primary service is to provide an income stream for the participant after they leave the workforce. In comparison to a 401(k), where employees can roll out and invest their own funds in any way they see fit to create a reliable income stream, employees with a pension are reliant on the investments the company makes. In recent years, due to a lack of funding or mismanagement, multiple pensions have reduced or frozen benefits to their employees. This has caused irreparable damage to employees who were relying on that income for most of their retirement funds.

Safety. We are all familiar with the ups and downs of the stock and bond markets. This is why 401(k) plans offer preset, diversified portfolios that help to minimize the long-term risk of investing. Pension funds invest their money in a similar way, but if that money is not managed or funded correctly, it can default. Pension plans typically insure themselves against failure through the Pension Benefit Guaranty Corporation (PBGC). However, this insurance protects only a fraction of those obligations, and it does not protect employees from reductions or freezes in their benefits. The PBGC, which is a federally chartered entity that insures these plans, is expected to use up its assets by the end of 2025 1.

Costs. A pension plan involves multiple organizations, each of which comes with its own unique set of costs. This may include hedge funds — which charge some of the highest fees in the financial industry — attorneys, actuaries, insurance companies and many others. These costs add up and impact the benefits offered.

Legacy planning. With a pension plan — if everything goes right — you will receive payments over your lifetime. Depending on the plan, the pension may offer reduced or no benefits to your spouse, or it may offer full spousal benefit, but only if you are willing to take a lower benefit when you start drawing your pension. In any of these scenarios, whatever is left in your pension account at the time of your death is returned to the fund. With a 401(k) plan, those assets are yours and can pass on to your children, enabling you to leave a legacy for your loved ones.

If you have any questions about the CoolSys retirement plan or preparing for retirement in general, please don’t hesitate to reach out to Nakell Lee at nakell.lee@coolsys.com or 714.853.4312.

The image above shows the funded ratio of some of the most underfunded pension plans for major corporations from 2017 2. Some of these companies have made huge reductions in their pension plan benefits in the years since 3. In the future, we may continue to see these names and others come up in the news.

1 https://www.pbgc.gov/news/press/releases/pr18-02

2 https://www.mymoneyblog.com/underfunded-private-pensions.html

3 https://www.ge.com/news/press-releases/ge-announces-us-pension-plan-actions#:~:text=1.,%2C%20effective%20January%201%2C%202021